The global electric vehicle market is currently accelerating on the fast track of development. According to the “Global Electric Vehicle Outlook 2022” released by the International Energy Agency (IEA), global sales of electric and plug-in hybrid vehicles reached a record 6.6 million units in 2021, doubling the previous year. Among them, electric vehicle sales have reached nearly 10% of global automobile sales, four times that of 2019. The IEA predicts that by 2030, electric vehicles will account for more than 30% of global automobile sales, reaching 200 million units.

From countries and regions to major commercial companies, everyone is flocking to electric vehicles. On the one hand, this is because they do represent the global trend of low-carbon ecological environmental protection and are a necessity. They will continue to develop on this right path. The acceleration is unmistakable. On the other hand, it is because the emergence of electric vehicles is a “big change unseen in a century” in the automobile industry. The unique system architecture of electric vehicles is likely to make the technical barriers and competitive advantages established by traditional car companies in the era of internal combustion engine vehicles no longer exist. This will also provide “latecomers” with the opportunity to overtake in corners. Therefore, in the field of electric vehicles, we always see many newcomers and crossover heavyweights.

A feast of automotive connectors.

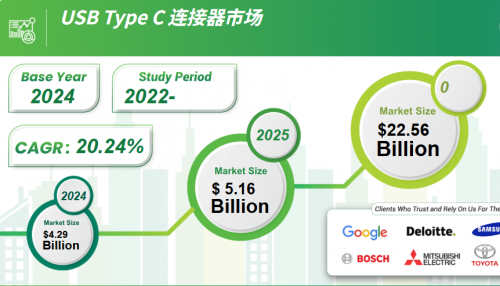

The heat from the electric vehicle market will naturally be transferred to the upstream electronic components industry. Taking connectors as an example, according to market research data from Bishop & Associates, global connector market sales will reach 62.73 billion yuan in 2020, of which the automotive connector market will reach US$14.15 billion. As early as 2019, the automotive field had surpassed the communications field and became the largest connector market segment with a 23.7% share. By 2025, driven by the demand for electric vehicles, the global automotive connector market will reach US$19.45 billion.

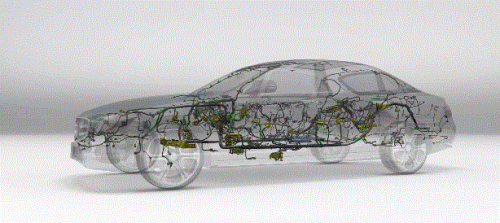

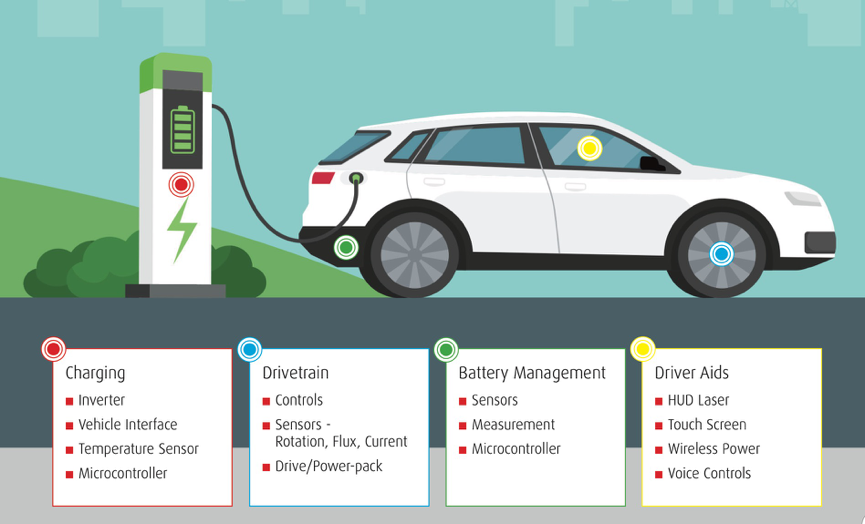

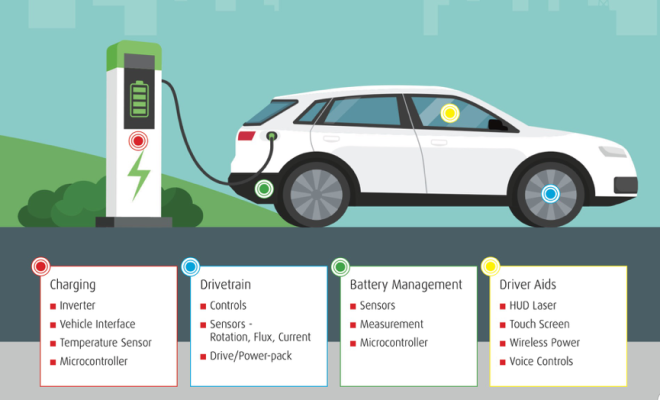

Currently, automotive connectors on the market can be mainly divided into three categories: low-voltage connectors, high-voltage connectors and high-speed connectors. Among them, low-voltage connectors are mainly used in body control fields such as braking systems, door wiring harnesses, gearboxes and steering systems in traditional automotive electronics. The development of the other two connectors is closely related to electric vehicles. Specifically, it is the electrification and intelligence of electric vehicles that promotes the rapid progress of high-voltage connectors and high-speed connectors.

In terms of electrification, unlike traditional fuel vehicles whose operating voltage is lower than 14V, the motor, battery, and electronic control “three power” systems of electric vehicles (including other new energy vehicles) require high voltage and large current to support higher power. . For example, it needs to reach voltage levels of 60V to 380V or higher and current levels of 10A to 300A. Nowadays, in order to support the “ultra-fast charging” experience, 800V battery packs are also used in electric vehicles – these new design requirements are bound to translate into increased demand for automotive high-voltage connectors.

In terms of intelligence, the introduction of increasingly rich functions such as ADAS and autonomous driving, Internet of Vehicles, smart cockpits, and new generation of Internet of Vehicles has caused an exponential increase in the data that electric vehicles need to process and transmit. At this time, only more Only high-speed connectors can keep up with this development trend and unleash the huge potential of data.

According to analysis, for traditional cars that mainly use low-voltage connectors, the connector value of each car is about 1,000 yuan. Thanks to the pull effect of electrification and intelligence, the value of bicycle connectors in electric vehicles will increase to 3,000 yuan to 5,000 yuan, and this figure can be as high as 8,000 yuan to 10,000 yuan in pure electric commercial vehicles.

From the perspective of macro market trends, taking the Chinese market, which accounts for half of the global electric vehicle market, as an example, analysts predict that China’s high-voltage connector market is expected to grow from 9.9 billion yuan in 2021 to 31.5 billion yuan in 2025, with a compound growth rate is 34%. The high-speed connector market size will grow from 3.2 billion yuan in 2021 to 15 billion yuan in 2025, with a compound growth rate of as high as 47%. Able to meet standard connectors.

The automotive connector market has broad room for development, but there are also barriers. Although according to this development trend, almost every subdivided connector category can find new development space in the field of electric vehicles. However, due to the particularity of automotive applications, this does not mean that any connector product can be “marketed”. “Used in automobiles. In other words, connectors that can meet the standards must be high-quality products that can withstand the rigorous test of automotive applications.

As far as electric vehicles are concerned, these severe tests are mainly reflected in the following aspects:

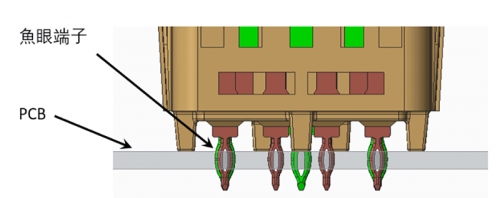

Reliability: The working environment of automobiles is complex. In order to ensure stable electrical interconnection under various application conditions, the connector needs to be specially designed to prevent mechanical vibration. The structure, material and process of the insulator and housing are specially optimized to ensure the stability of the connector and PCB assembly. sex.

Anti-interference: More and more electronic products will be introduced into electric vehicles, especially the introduction of high-power power supplies and wireless communication equipment, which will make the electromagnetic environment of vehicles more complex. Therefore, higher requirements will also be placed on related connector products in terms of electromagnetic compatibility design and signal integrity.

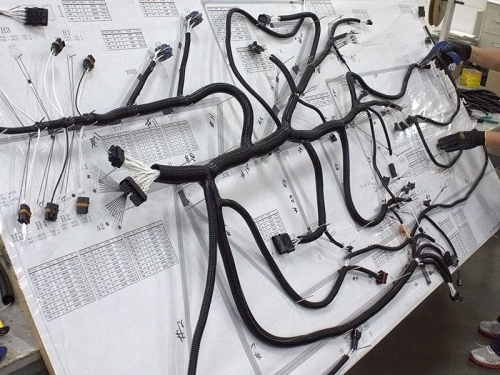

Miniaturization: The space provided by automobiles is limited, which makes the design of automobile electronic systems a difficult problem. Obviously, within this limitation, miniaturization and high-density connectors will be more popular.

Easy installation: The ever-increasing number of connectors and limited space have raised user requirements for ease of assembly operations to unprecedented heights. Preventing mating errors and providing a simpler assembly experience through polarized designs and other methods are technology choices that need to be carefully considered when designing automotive connectors.

Only if the main electrical and mechanical characteristics meet the requirements of the design specifications and can meet the above-mentioned harsh conditions can such connector products be selected.